Three company-specific sources can drive positive total returns for stock investors: growth in earnings, growth in the collective price investors are willing to pay for those earnings (“multiple expansion”), and dividends the investor receives from the companies they own.

At times, earnings growth and multiple expansion dominate the total return picture. Growth stocks reign and dividend-paying stocks can be cast aside, as the dividend’s role is minimized. During such periods, we believe that it is prudent to revisit the enduring strength of dividend-paying companies, though, not all are alike.

When investing in dividend-paying stocks, it is critical to maintain a minimum quality threshold rather than simply reaching for the highest-yielding companies. Foregoing the highest-yielding one-fifth of stocks in favor of the group just below helps investors narrow their search for companies that meet the quality test.

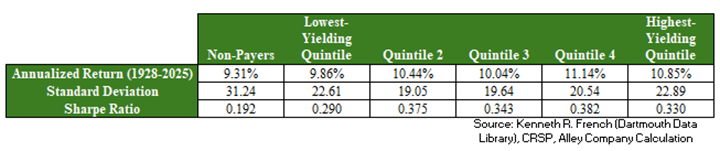

For nearly a century, such stocks have delivered relatively outsized gains and a smoother ride. The below table depicts the range of performance for dividend-paying U.S. stocks broken out into five buckets (from those yielding the most to those yielding the least), plus an additional bucket for non-dividend paying U.S. stocks. The data show that from 1928 through 2025, the second-highest yielding group of companies produced the best absolute return and with comparatively lower volatility, as measured by standard deviation. This resulted in the highest Sharpe ratio, a risk-adjusted performance metric, for the group.

Part of this superior risk-adjusted performance came from the cohort’s tendency to hold up better during market selloffs. In the graph below, we ranked the percentage of months that each aforementioned cohort placed as one of the worst two performers amongst the group during months when the broad market fell more than three percent. Once again, the second highest-yielding quintile was best-in-show. At the same time, those companies that paid no dividend, or paid a relatively low dividend, consistently ranked near the bottom. It is also noteworthy that the highest-yielding group often stacked up poorly during months of market stress, proving that there is risk when reaching for yield.

The preceding data indicates that, while investing in dividend-paying companies broadly has been an attractive proposition, not all dividend-payers are created equal. Hunting for stocks near the middle of the dividend-paying pack has proven to be fertile ground in the search for quality companies, which is why it has been central to our investment approach at Alley Company for nearly two decades.

Quality is subjective. But, an abbreviated summary of our definition includes companies that maintain prudent levels of debt, are leaders within the markets they serve, have a proven track record of favorable financial results, and leadership teams composed of sound decision-makers. Companies that exhibit these characteristics are often better positioned to weather the storm when the good times in the economy inevitably reverse.

Those stocks that are further down the quality spectrum are more susceptible to grappling with slowing sales and shrinking operating earnings. They also lack flexibility when struck with this painful combination. Excessive debt levels act like an anchor, compelling management teams to cut the company’s dividend in order to maintain interest payments and avoid default. The mirage of the company’s once-seemingly attractive dividend yield now looks less appealing.

Alternatively, not all, but certain companies that pay no dividend at all can lack the financial discipline that adhering to a regimented dividend program often brings. Excess cash flow may be funneled toward endeavors with low prospects of generating an attractive rate of return.

On the whole, it has paid to stick closer to the middle of the dividend-paying pack of stocks rather than reaching for yield or holding only those companies that pay no dividend at all. This is a foundational guidepost of our investment philosophy. It has stood the test of time through the past century, and we believe it will stand in the decades to come.

March 2026

The Alley Company Commentary discusses general developments, financial events in the news and investment principles. It is provided for information purposes only. It does not provide investment advice and is not an offer to sell a security or a solicitation of an offer, or a recommendation, to buy a security. The statements and opinions contained herein are solely those of Alley Company and are based upon sources and data believed to be accurate and reliable. Additional information regarding Alley Company can be found by accessing the SEC’s website at www.adviserinfo.sec.gov.