A phrase that is often used within investing is “risk-adjusted returns,” meaning how much risk was taken to achieve the return. While investors should have equal focus on both risk and return, human nature dictates that attention tends to swing from one to the other as market conditions change. At the depths of bear markets, investors are understandably fixated on real and perceived risks. But during bull markets, their focus turns to potential return and the seemingly unending blue sky.

In today’s bull market cycle, investors need to keep an eye on potential risks, including the elevated level of concentration risk within certain market indices, sectors, and individual stocks. In this letter, we touch upon these risks as well as opportunities for investors.

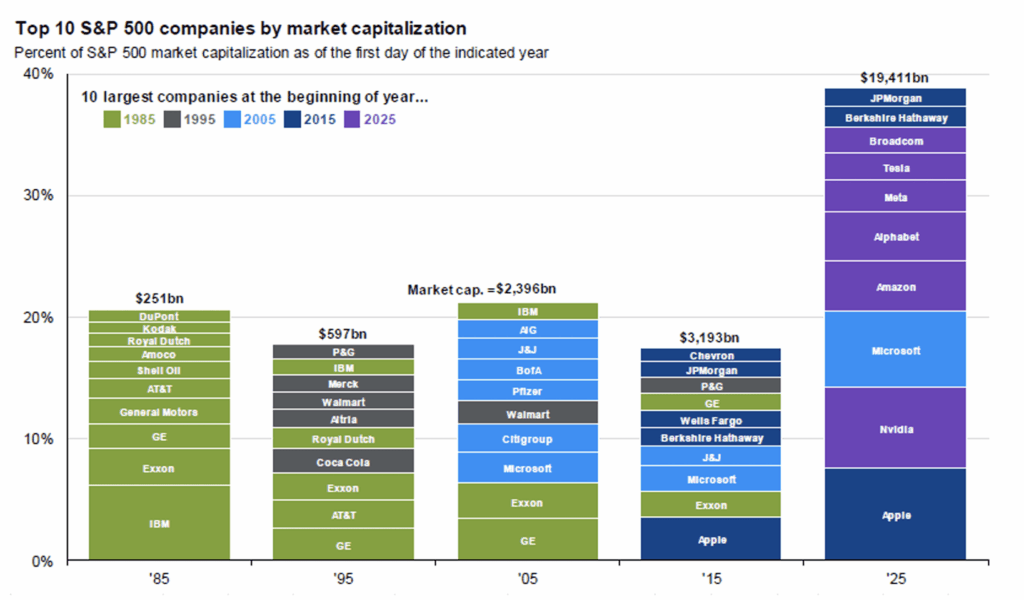

To be sure, many technology and technology-related companies have had a remarkable run of operational performance over the past decade. Earnings growth for these companies has been brisk and, as a result, their market capitalizations have expanded to the point where they now occupy a large portion of the S&P 500 index. Presently, over 20% of the index is derived from just three companies – Nvidia, Apple, and Microsoft. If one adds Alphabet, Amazon, and Meta Platforms, then these six companies represent over 30% of the index.

The technology sector overall is nearing 35% of the index, and if “tech-related” companies are factored in, then the concentration is closing in on 50% of the popular index! As a result, a traditionally passive investment in the S&P 500 index has increasingly become an outsized bet on technology-related companies. This level of concentration, by definition, challenges the general principles of diversification within investment portfolios.

The chart on the following page depicts the current composition of the top ten largest companies within the S&P 500 index, along with a snapshot of the past four decades. Looking back, the ten largest companies typically amount to roughly 20% of the index. Today’s ten largest companies comprise nearly 40% of the index.

A natural question is: “what is causing the increased concentration within sectors and individual companies?” Among others, three important drivers are 1) the rapid proliferation of cloud computing use within organizations, 2) a step forward in technology adoption by both consumers and corporations to navigate the Covid-19 pandemic, and 3) the dramatic rise of artificial intelligence (AI) spending since 2022. As it relates to the latter, JP Morgan noted, “AI related stocks have accounted for 75% of the S&P 500 returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November of 2022.” Cloud computing and Covid-19 sped up technology adoption, but the rise of artificial intelligence is currently turbocharging the industry.

Artificial intelligence, if used productively, holds tremendous promise and opportunity for society and is likely to change virtually every business and industry. This current phase is marked by a profound level of investment. According to Gartner, worldwide spending on AI is estimated to be $1.5 trillion in 2025, a staggering sum. In the U.S. alone, Alphabet, Amazon, Meta, and Microsoft are estimated to spend north of $300 billion just this year.

The buildout of AI may follow a similar path as the dawn of the Internet in the late 1990s. First, there was a substantial investment to lay the foundation, then a shakeout period where unsustainable business models faltered, and eventually came a time when the technology provided lasting economic benefit to society along with select companies that clearly prospered. Presently, the return on capital invested to date has been negligible and this will have to improve for the AI capital expenditure boom to continue. Investors needed to be discerning during the late 1990s as the Internet-era unfolded, and we believe the same approach is necessary today.

Balancing both risk and return is paramount to generating attractive, risk-adjusted returns over the long term. Accordingly, discipline around company and sector weightings, along with overall portfolio diversification, have been key components for Alley Company in building portfolios for our clients. While the promise of artificial intelligence is real and certain businesses will benefit, risks within markets require attention due to record high levels of concentration in individual companies and sectors. Portfolio diversification has been called “the only free lunch in investing” and we believe investors should be mindful of this advice in today’s market environment.

The Alley Company Quarterly Letter discusses general developments, financial events in the news and investment principles. It is provided for information purposes only. It does not provide investment advice and is not an offer to sell a security or a solicitation of an offer, or a recommendation, to buy a security. The statements and opinions contained herein are solely those of Alley Company and are based upon sources and data believed to be accurate and reliable. Additional information regarding Alley Company can be found by accessing the SEC’s website at www.adviserinfo.sec.gov.